美國退休老人開始縮減開支

Megan Leonhardt

2022-11-27

退休儲蓄遭受一次又一次的打擊。

文本設置

文本設置

Plus(0條)

Plus(0條)

安妮塔·考爾斯計劃于明年乘坐游輪暢游歐洲,領略距離她的家鄉美國阿拉巴馬州數千英里之外的風光,那里的各大城市充滿活力、宮殿鱗次櫛比,還能夠參觀中世紀的堡壘。

然后,她和丈夫拉塞爾計劃開著他們的新房車進行為期三個月的公路旅行。這只是拉塞爾在今年2月年滿65歲從美國航空公司(American Airlines)退休后,這對夫婦計劃的眾多旅行中的兩次旅行。

但這一切都被擱置了,部分原因是汽油價格高企、消費品價格上漲,以及市場低迷吞噬了這對夫婦約四分之一的退休儲蓄。63歲的安妮塔對《財富》雜志表示,自今年2月以來,這對夫婦的投資損失了約50萬美元。

“那是我們退休儲蓄的一大筆錢。”安妮塔說。“這非常可怕。我們原以為今年會去旅游,但這一切都戛然而止。你希望你的錢可以長久保值。”

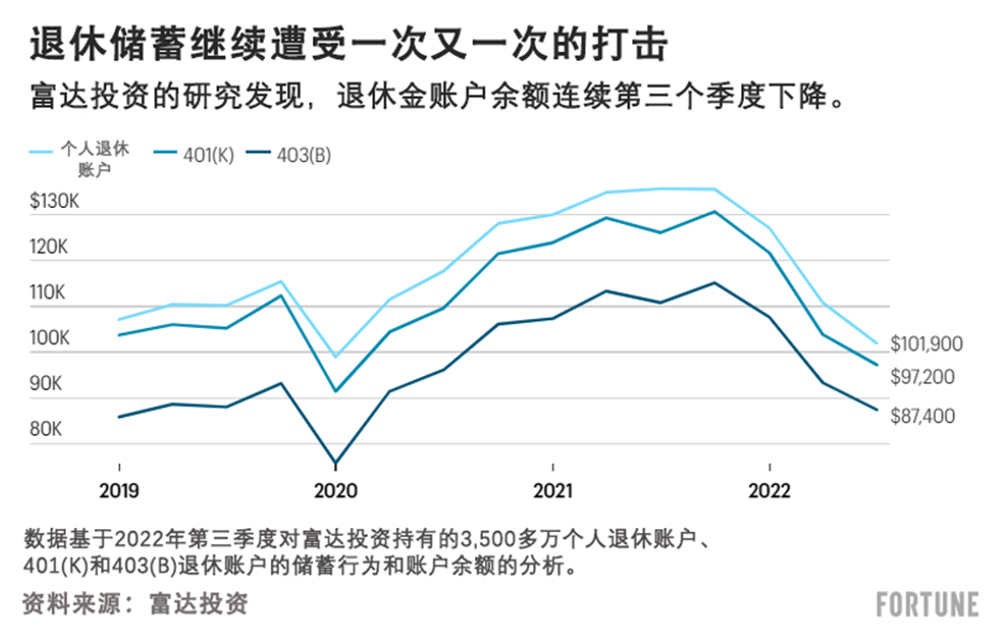

考爾斯夫婦并不是唯一面臨重大損失的人,他們的退休金余額連續第三個季度下降。富達投資(Fidelity Investments)最近的研究顯示,在第三季度,富達投資的401(k)(企業年金計劃)退休金余額較上年同期平均下降23%。富達投資管理著約3,500萬個退休賬戶。個人退休賬戶(IRA)余額同比下降了近25%,403(b)賬戶所持股份(通常由非營利組織提供的退休計劃)減少了21%。

盡管在投資者提款之前,這些下跌只是賬面損失,但心理作用已經在打擊像考爾斯夫婦這樣剛退休或者即將退休的人。安妮塔稱:“是的,這只是賬面上的損失,但如果你一直從賬上提款,那么你就要花更長的時間才能夠回本。”

最近的市場低迷和不斷上升的通貨膨脹讓許多美國老年人躊躇不前。根據Janus Henderson Investors近期發布的《Janus 2022退休信心報告》(Janus 2022 Retirement Confidence Report),在50歲及以上的人群中,近一半(49%)的人表示,由于這些因素,他們已經減少了支出,或者計劃這樣做。

然而,許多人還是很樂觀,他們認為,通脹和市場低迷是短期挑戰。Janus的數據顯示,大多數的美國老年人(60%)認為,一年后標準普爾500指數(S&P 500)將走高。考慮到嬰兒潮一代普遍都可以在過去的經濟沖擊中重振旗鼓——特別是與其他幾代人相比。根據美聯儲(Federal Reserve)的數據,雖然嬰兒潮一代經歷了20世紀90年代末的互聯網泡沫和2008年的股市和樓市崩盤,但這一代的財富約為730億美元,約占美國全部財富的51%,大約是千禧一代財富的9倍。

安妮塔指出:“我知道在未來一兩年里,我能夠進行規劃中的某些旅行,因為會回本的。”但仍然有不確定性的陰影在逼近。因此,為了盡快挽回損失,考爾斯夫婦一直在討論讓拉塞爾回到一家較小的航空公司當飛行員。就在上周,他還在面試一個職位。“他正在考慮回去工作,因為如果這種情況繼續下去的話,怎么辦呢?”安妮塔表示。

她說:“我們最失望的是這一切發生的時機。”她補充道,當需要考慮長期健康問題時,需要做的更大的決定是推遲旅行和拉塞爾可能不退休。她還表示:“我們仍然過得很舒適。”但她指出,所有的“額外花銷”,比如旅行和特殊體驗,這對夫婦想要在經濟寬裕的情況下進行體驗,但現在他們無法體驗了。

如何在不退休的情況下度過難關

雖然重返工作崗位的決定(即便是兼職)并不是一種壞的沖動,但還有其他方法可以抵御高通脹和市場低迷的雙重打擊,這是正在退休的嬰兒潮一代和已經退休的嬰兒潮一代正在經歷的。

T. Rowe Price公司的研究發現,即便是在市場和經濟形勢嚴峻時期開始的退休儲蓄也能夠長期維持下去。例如,在1973年投資50萬美元的60/40股票和債券投資組合——這一年石油危機引發了熊市——以4%的提款率計算,30年后的結余仍然超過100萬美元。

但這類研究并不意味著最近退休的嬰兒潮一代(或者仍然在考慮退休的人)應該自滿,伊利諾斯州的Bentron金融集團(Bentron Financial Group)的注冊理財規劃師格雷戈里·庫里尼克表示。

“是時候退一步,做你應該做的事情了。”庫里尼克說。當務之急是什么?重新評估你每月和每年的實際支出。然后想一想,在當前嚴峻的市場環境下,這些收入將從哪里來。

即便是這樣簡單的練習,也需要權衡很多要素。位于紐約的Siena Private Wealth的注冊理財規劃師和個人理財顧問瑪麗莎·羅斯坦說:“通常的原則是,當投資組合下跌時,你不應該回撤。”

這一原則的自然延伸是,退休前和退休人員應該依靠其他收入來源度過難關,直到市場復蘇——最常見的收入來源是社會保障金。但如果這意味著提前領取社會保障金(大多數嬰兒潮一代的法定退休年齡是66歲或67歲),羅斯坦稱,這就可能是一個糟糕的賭注。如果提前領取社會保障金,他們就很可能失去每推遲一年退休,社會保障金的預期增長。股市可能會反彈,但它會以每年8%的速度反彈嗎?我們無法預測。但我們可以肯定的是,你在達到法定退休年齡后,每推遲一年退休,你的社會保障金就會以8%的速度增長,你的社會保障金將持續增長直到你年滿70歲。”

比如,庫里尼克建議他的客戶利用一兩年的儲蓄建立一個進入退休的匝道,而不是依賴社會保障金或者投資提款。儲蓄賬戶余額不會給投資者帶來高額回報,但現在使用這些資金而不是動用退休賬戶,意味著那些投資將更有機會回本,你能夠推遲領取社會保障金。賬面損失轉化為現實損失的機會就更少。

“如果你的計劃已經就位,那么你就應該可以抵御像這樣的風暴。”庫里尼克說。“你猜怎么著,這不是我們要經歷的最后一場風暴。”

對退休的成本要現實一點

帶著合乎實際的期望進入退休生活也是關鍵。關于退休最大的誤解之一是,退休后需要的錢比工作時要少。庫里尼克說,這種認識是錯誤的。

像考爾斯夫婦一樣,許多美國人想去旅行或做所有因為工作而無法做的事情。庫里尼克表示,他接觸過的最近退休的人員通常比停止全職工作前多支出105%到110%,而且這種情況可能會持續到退休后的五年或十年。

同樣,另一個巨大的障礙是,退休人員將自動處于較低的稅率等級。庫里尼克再次指出,這通常不會立即發生。他說:“如果我們花更多的錢,就意味著我們提取更多的錢,這意味著我們可能會處于同等的,甚至是更高一點的稅率等級。”更不用說目前美國的稅率可能是許多美國人所見過的最低稅率。

庫里尼克表示,盡管他從不建議客戶不做某件事情,例如在投資組合縮水23%的時候就不去遠行,但他確實強調了潛在的后果,以及可能需要優先考慮的重要事情。妥協。靈活處理。他補充道,這些原則將很好地幫助那些退休后進入這種環境的人。“一切都在變化。計劃是不斷變化的——事情一直在變化。”

然而,不管怎么說,庫里尼克強調了制定計劃的重要性。他說:“這并不意味著每個人都需要與理財規劃師合作,但你需要制定某種計劃,并確保該計劃是可靠的。”

每個人對退休的定義都是不同的,但所有這些都意味著不同額度的消費,這有助于你很好地理解你可以通過做哪些事情來實現既定的目標。(財富中文網)

譯者:中慧言-王芳

安妮塔·考爾斯計劃于明年乘坐游輪暢游歐洲,領略距離她的家鄉美國阿拉巴馬州數千英里之外的風光,那里的各大城市充滿活力、宮殿鱗次櫛比,還能夠參觀中世紀的堡壘。

然后,她和丈夫拉塞爾計劃開著他們的新房車進行為期三個月的公路旅行。這只是拉塞爾在今年2月年滿65歲從美國航空公司(American Airlines)退休后,這對夫婦計劃的眾多旅行中的兩次旅行。

但這一切都被擱置了,部分原因是汽油價格高企、消費品價格上漲,以及市場低迷吞噬了這對夫婦約四分之一的退休儲蓄。63歲的安妮塔對《財富》雜志表示,自今年2月以來,這對夫婦的投資損失了約50萬美元。

“那是我們退休儲蓄的一大筆錢。”安妮塔說。“這非常可怕。我們原以為今年會去旅游,但這一切都戛然而止。你希望你的錢可以長久保值。”

考爾斯夫婦并不是唯一面臨重大損失的人,他們的退休金余額連續第三個季度下降。富達投資(Fidelity Investments)最近的研究顯示,在第三季度,富達投資的401(k)(企業年金計劃)退休金余額較上年同期平均下降23%。富達投資管理著約3,500萬個退休賬戶。個人退休賬戶(IRA)余額同比下降了近25%,403(b)賬戶所持股份(通常由非營利組織提供的退休計劃)減少了21%。

盡管在投資者提款之前,這些下跌只是賬面損失,但心理作用已經在打擊像考爾斯夫婦這樣剛退休或者即將退休的人。安妮塔稱:“是的,這只是賬面上的損失,但如果你一直從賬上提款,那么你就要花更長的時間才能夠回本。”

最近的市場低迷和不斷上升的通貨膨脹讓許多美國老年人躊躇不前。根據Janus Henderson Investors近期發布的《Janus 2022退休信心報告》(Janus 2022 Retirement Confidence Report),在50歲及以上的人群中,近一半(49%)的人表示,由于這些因素,他們已經減少了支出,或者計劃這樣做。

然而,許多人還是很樂觀,他們認為,通脹和市場低迷是短期挑戰。Janus的數據顯示,大多數的美國老年人(60%)認為,一年后標準普爾500指數(S&P 500)將走高。考慮到嬰兒潮一代普遍都可以在過去的經濟沖擊中重振旗鼓——特別是與其他幾代人相比。根據美聯儲(Federal Reserve)的數據,雖然嬰兒潮一代經歷了20世紀90年代末的互聯網泡沫和2008年的股市和樓市崩盤,但這一代的財富約為730億美元,約占美國全部財富的51%,大約是千禧一代財富的9倍。

安妮塔指出:“我知道在未來一兩年里,我能夠進行規劃中的某些旅行,因為會回本的。”但仍然有不確定性的陰影在逼近。因此,為了盡快挽回損失,考爾斯夫婦一直在討論讓拉塞爾回到一家較小的航空公司當飛行員。就在上周,他還在面試一個職位。“他正在考慮回去工作,因為如果這種情況繼續下去的話,怎么辦呢?”安妮塔表示。

她說:“我們最失望的是這一切發生的時機。”她補充道,當需要考慮長期健康問題時,需要做的更大的決定是推遲旅行和拉塞爾可能不退休。她還表示:“我們仍然過得很舒適。”但她指出,所有的“額外花銷”,比如旅行和特殊體驗,這對夫婦想要在經濟寬裕的情況下進行體驗,但現在他們無法體驗了。

如何在不退休的情況下度過難關

雖然重返工作崗位的決定(即便是兼職)并不是一種壞的沖動,但還有其他方法可以抵御高通脹和市場低迷的雙重打擊,這是正在退休的嬰兒潮一代和已經退休的嬰兒潮一代正在經歷的。

T. Rowe Price公司的研究發現,即便是在市場和經濟形勢嚴峻時期開始的退休儲蓄也能夠長期維持下去。例如,在1973年投資50萬美元的60/40股票和債券投資組合——這一年石油危機引發了熊市——以4%的提款率計算,30年后的結余仍然超過100萬美元。

但這類研究并不意味著最近退休的嬰兒潮一代(或者仍然在考慮退休的人)應該自滿,伊利諾斯州的Bentron金融集團(Bentron Financial Group)的注冊理財規劃師格雷戈里·庫里尼克表示。

“是時候退一步,做你應該做的事情了。”庫里尼克說。當務之急是什么?重新評估你每月和每年的實際支出。然后想一想,在當前嚴峻的市場環境下,這些收入將從哪里來。

即便是這樣簡單的練習,也需要權衡很多要素。位于紐約的Siena Private Wealth的注冊理財規劃師和個人理財顧問瑪麗莎·羅斯坦說:“通常的原則是,當投資組合下跌時,你不應該回撤。”

這一原則的自然延伸是,退休前和退休人員應該依靠其他收入來源度過難關,直到市場復蘇——最常見的收入來源是社會保障金。但如果這意味著提前領取社會保障金(大多數嬰兒潮一代的法定退休年齡是66歲或67歲),羅斯坦稱,這就可能是一個糟糕的賭注。如果提前領取社會保障金,他們就很可能失去每推遲一年退休,社會保障金的預期增長。股市可能會反彈,但它會以每年8%的速度反彈嗎?我們無法預測。但我們可以肯定的是,你在達到法定退休年齡后,每推遲一年退休,你的社會保障金就會以8%的速度增長,你的社會保障金將持續增長直到你年滿70歲。”

比如,庫里尼克建議他的客戶利用一兩年的儲蓄建立一個進入退休的匝道,而不是依賴社會保障金或者投資提款。儲蓄賬戶余額不會給投資者帶來高額回報,但現在使用這些資金而不是動用退休賬戶,意味著那些投資將更有機會回本,你能夠推遲領取社會保障金。賬面損失轉化為現實損失的機會就更少。

“如果你的計劃已經就位,那么你就應該可以抵御像這樣的風暴。”庫里尼克說。“你猜怎么著,這不是我們要經歷的最后一場風暴。”

對退休的成本要現實一點

帶著合乎實際的期望進入退休生活也是關鍵。關于退休最大的誤解之一是,退休后需要的錢比工作時要少。庫里尼克說,這種認識是錯誤的。

像考爾斯夫婦一樣,許多美國人想去旅行或做所有因為工作而無法做的事情。庫里尼克表示,他接觸過的最近退休的人員通常比停止全職工作前多支出105%到110%,而且這種情況可能會持續到退休后的五年或十年。

同樣,另一個巨大的障礙是,退休人員將自動處于較低的稅率等級。庫里尼克再次指出,這通常不會立即發生。他說:“如果我們花更多的錢,就意味著我們提取更多的錢,這意味著我們可能會處于同等的,甚至是更高一點的稅率等級。”更不用說目前美國的稅率可能是許多美國人所見過的最低稅率。

庫里尼克表示,盡管他從不建議客戶不做某件事情,例如在投資組合縮水23%的時候就不去遠行,但他確實強調了潛在的后果,以及可能需要優先考慮的重要事情。妥協。靈活處理。他補充道,這些原則將很好地幫助那些退休后進入這種環境的人。“一切都在變化。計劃是不斷變化的——事情一直在變化。”

然而,不管怎么說,庫里尼克強調了制定計劃的重要性。他說:“這并不意味著每個人都需要與理財規劃師合作,但你需要制定某種計劃,并確保該計劃是可靠的。”

每個人對退休的定義都是不同的,但所有這些都意味著不同額度的消費,這有助于你很好地理解你可以通過做哪些事情來實現既定的目標。(財富中文網)

譯者:中慧言-王芳

Anita Cowles planned to be on a river cruise in Europe next year, taking in the sights and sounds of vibrant cities, sprawling palaces, and medieval fortresses thousands of miles away from her Alabama hometown.

She and her husband, Russell, then planned to undertake a three-month roadtrip in their new RV. Those are just two of the many trips the couple were planning after Russell retired as a pilot from American Airlines in February when he turned 65.

But all of that has been put on hold in part because of high gas prices, higher consumer goods prices, and a market downturn that’s wiped out about a quarter of the couple’s retirement savings. Since February, the couple’s investments have lost about $500,000 in value, Anita, 63, tells Fortune.

“That’s a big chunk of our retirement,” Anita says. “It’s extremely scary. We thought that we would be doing some traveling this year, but that’s come to an abrupt halt. You want your money to last.”

The Cowles aren’t alone in facing major losses—retirement balances dipped for the third consecutive quarter this year. During the third quarter, the average 401(k) balance at Fidelity dropped an average of 23% from a year ago, according to recent Fidelity Investments research, which handles about 35 million retirement accounts. IRA balances dropped nearly 25% year-over-year and 403(b) account holdings—retirement plans typically used by nonprofits—were down 21%.

While these dips are merely paper losses until investors make withdrawals, the psychological effects are already hitting recent and pre-retirees like the Cowles. “Yes, it is just on paper, but if you keep drawing from that, then it’s going to take even longer to make your money back,” Anita says.

The recent market downturn and rising inflation have given many older Americans pause. Nearly half (49%) of those ages 50 and older report they have already reduced their spending, or plan to do so, as a result of these factors, according to Janus Henderson Investors’ recent Janus 2022 Retirement Confidence Report.

Yet, many are optimistic that inflation and down markets are short-term challenges. A majority of older Americans (60%) believe the S&P 500 Index will be higher one year from now, according to Janus. And that tracks, given that baby boomers are a generation that has generally recovered nicely from economic shocks in the past—especially compared to other generations. While baby boomers experienced the Dot Com bubble in the late 1990s and the stock market and housing crash of 2008, the generation holds about $73 billion, or about 51% of all the U.S. wealth, according to the Federal Reserve. That’s about nine times more than millennials.

“I know that ahead a year or two, I’ll be able to take some of those trips because the money will be back,” Anita says. But there’s still a shadow of uncertainty looming. So in an effort to recoup some of their losses faster, the Cowles have been discussing Russell returning to work as pilot for a smaller airline. Just last week he was interviewing for a role. “He’s considering going back to work because what if it continues?” Anita says.

“Our biggest disappointment really is just the timing of all this,” she says, adding that delaying trips and Russell potentially unretiring are bigger decisions when there are long-term health concerns to weigh. “We are still comfortable,” she adds but says that all of the “extras” like travel and special experiences the couple wanted to be able to do while feeling okay financially about it—now they can’t.

How to weather the storm without coming out of retirement

While the decision to head back to work, even on a part-time basis, isn’t a bad impulse, there are other ways to weather the double whammy of high inflation and a down market that retiring and retired baby boomers are experiencing.

Research from T. Rowe Price finds that retirement savings do hold up over the long haul, even when starting in challenging market and economic periods. A $500,0000 retirement savings in a 60/40 portfolio of stocks and bonds, for example, invested in 1973—a year marked by an oil crisis that kicked off a bear market—still ended up with a balance of more than $1 million at the end of 30 years using a 4% withdrawal rate.

But that kind of research doesn’t mean recently retired baby boomers (or those still eying retirement) should be complacent, says Gregory Kurinec, a certified financial planner (CFP) with Illinois-based Bentron Financial Group.

“It’s time to take a step back and do the things that you’re supposed to do,” Kurinec says. The top priority? Reevaluate how much you’re actually spending on a monthly and annual basis. Then figure out where that income is going to come from given the current tough market climate.

Even with that simple exercise, there are a lot of tradeoffs to consider. “The common wisdom is that you should never pull out of your portfolio when it is down,” says Marisa Rothstein, a CFP and personal financial advisor at New York-based Siena Private Wealth.

The natural extension of this wisdom is that pre-retirees and retirees should rely on other sources of income to get them through until the market recovers—the most common go-to source being Social Security. But if that means claiming Social Security early (full retirement age is 66 or 67 for most baby boomers), Rothstein says it could be a bad bet. “By claiming Social Security early, they are likely forfeiting the promised growth built into Social Security from each year of delay. The stock market might rebound, but will it rebound at a rate of 8% per year? We just can’t predict that. But we can be sure that your Social Security benefit will grow at that rate for every year you postpone beyond your full retirement age. And will continue to grow until age 70.”

Kurinec, for instance, recommends his clients build an on-ramp into retirement using a year or two of savings, rather than relying on Social Security or withdrawals from investments. A savings account balance isn’t going to net investors a ton of return, but using these funds now instead of dipping into retirement accounts means that those investments will have a better chance of recovering and you can hold off on claiming Social Security. Less chance of paper losses turning into realized losses.

“If you have a plan in place, then you should be able to weather storms like this,” Kurinec says. “And guess what, this isn't the last one we're gonna go through.”

Be realistic about the cost of being a retiree

Going into retirement with realistic expectations is also key. One of the biggest misconceptions about retirement is that Americans need less money in retirement than while they’re working. Wrong, Kurinec says.

Like the Cowles, many Americans want to travel or do all the things they weren’t able to do because they were working. Kurinec says recent retirees he works with typically end up spending 105% to 110% more than what they were spending before they stopped working full-time—and that can last for five or 10 years after retirement.

In that same vein, another huge stumbling block is the idea that retirees are going to automatically be in a lower tax bracket. Again, Kurinec says that generally doesn’t happen right away. “If we're spending more money, that means we're taking in more money, which means we're probably gonna be in an equal, if not a little bit of a higher tax bracket,” he says. Not to mention that the current U.S. tax rates are probably the lowest many Americans are ever going to see.

Kurinec says that while he never tells his clients not to do something, like take a big trip when their portfolio is down 23%, he does stress the potential consequences and the need to perhaps prioritize what’s important. Compromise. Be flexible. Those tenets will serve folks who are retiring into this environment well, he adds. “Everything is fluid. Planning is fluid—things change all the time,” he says.

At the end of the day however, Kurinec stresses the importance of having a plan. “That doesn't mean every single person needs to work with a financial planner, but you need to have some sort of plan in place and make sure that plan is solid,” he says.

Everybody's definition of retirement is going to be different, but that's all going to cost different amounts of money, and it helps to have a good grasp on what you want to do to make that a reality.

請打開財富Plus APP