別怪亞馬遜,零售巨頭西爾斯轟然倒下只能怪自己

|

據《華爾街日報》報道,西爾斯控股已經聘請顧問,可能按照美國破產法第11章遞交破產申請。即使是不了解零售業的人,聽到消息也會感到吃驚。 如今的西爾斯控股是兩大美國零售業巨頭西爾斯和Kmart合并的產物,已然負債累累。2004年,前對沖基金大王艾迪·萊姆伯特撮合兩家公司合并,卻顯然欠考慮。合并后的西爾斯業績連年萎靡,既未能在零售業的新領域立足,也沒能通過投資實體店和商品提振經營。 上周,西爾斯有高達1.34億美元債務到期。公司一度股價跌至0.44美元,僅僅12年前股價還曾觸及145美元高點。西爾斯未對破產保護申請的可能性置評。但上周該公司董事會的確增加了一名擁有企業重組經驗的董事。 2013年,西爾斯的首席執行官走馬燈一般更迭后,終于確定由萊姆伯特接任。過去幾年,他為了還債出售公司很多優質業務,包括業績最好的一些門店、Lands’ End和Craftsman之類知名品牌、(去年清算的)遍布加拿大的龐大百貨公司網。事實證明,不管是大甩賣,還是萊姆伯特旗下對沖基金提供的大筆貸款,都很難阻止西爾斯走向末路。而且出售業務無異于飲鴆止渴,西爾斯還失去了有機會在競爭中脫穎而出的特色。畢竟,零售商玩資本運作幾時有過好結果? 盡管十年里關閉了幾百家門店,西爾斯和Kmart仍然每況愈下,近年來同店銷售持續下滑。事實上,從2005年開始,希爾斯控股已經不再公布單一年份的銷售和同店(剔除新開張或關閉門店影響)銷售增長數據。2011年年初以來,該公司累計凈虧損112億美元。隨著西爾斯的業務越變越少,業績也日漸慘淡,重拾昔日榮光的機會也逐漸渺茫。2015年,公司年營業收入還有540億美元,而到了2018年,華爾街預計其年收入僅有124億美元。 |

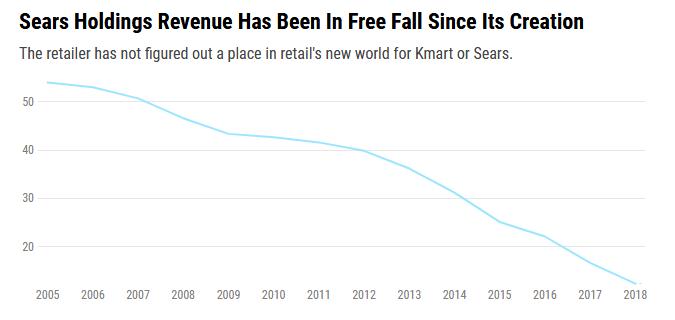

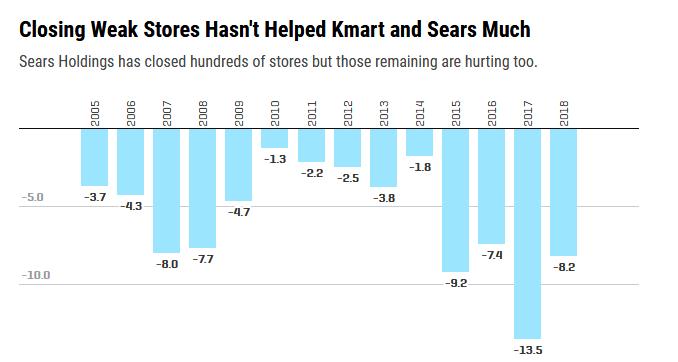

The Wall Street Journal report published late Tuesday saying Sears Holdings (shld, -23.19%) has hired advisers ahead of a potential Chapter 11 bankruptcy filing this week came as a surprise to no one following the retail industry even remotely closely. The company, a debt-laden retail Frankenstein begat from the ill-advised merger of Kmart and Sears engineered in 2004 by former hedge fund king Eddie Lampert, has been withering for years, unable to find a place for itself in retail’s new world or help itself by investing in its stores and merchandise. Sears, which has $134 million in debt coming due last week, saw shares plummet to $0.44; shares were at $145 at the company’s peak only 12 years ago. The company did not respond to a request for comment on the prospect of a bankruptcy protection filing, but last week the company did add a board member with corporate restructuring experience. To keep Sears solvent in the last few years, Lampert, who became CEO in 2013 after endless turnover in the corner office, has sold off many of Sears’ crown jewels, including its best stores, brands like Lands’ End and Craftsman, and its once-large Canadian unit (which liquidated last year). Those, along with quite a few loans Lampert has made via his hedge fund, have proven to be temporary salves to keep Sears from going under. But ultimately, they hurt the retailer by depriving it of the very features that helped it stand out from rivals. After all, since when has financial engineering ever made a retailer more attractive? Despite closing hundreds of stores this decade, Sears and Kmart both continued to deteriorate, with same-store declines worsening in the last few years. In fact since 2005, Sears Holdings has not reported a single year of sales or comparable sales (which strip out the impact of newly closed or opened stores) growth. The company has rung up $11.2 billion in cumulative net losses since the start of 2011. So much for a leaner and meaner Sears getting its mojo back. In 2015, Sears Holdings had annual revenue of $54 billion. For 2018, Wall Street expects it to come in at $12.4 billion. |

|

慢性惡化的根源在哪里?首先,西爾斯沒能吸引購物者不斷上門,Kmart也沒有。誰能想到,就在三十年前,Kmart曾是比沃爾瑪更大的零售商。西爾斯旗下太多的門店非常陳舊,與此同時,塔吉特、沃爾瑪和(奪走西爾斯眾多家電業務份額的)家得寶都在門店和技術方面投入巨資。西爾斯當年在商品目錄銷售領域稱霸一時,本可以在電子商務的戰場上取勝,卻拋棄了優勢。在開拓商品業務方面,西爾斯遠沒有競爭對手積極主動:除了幾年前因銷售不佳而撤柜的金·卡戴珊自創時裝品牌Kardashian Kollection,誰還記得西爾斯出售過哪些牌子的服裝? 萊姆伯特承諾的改進遲遲未落實,他堅持將西爾斯改造成會員制零售商,努力打造會員項目ShopYourWay。按照這種路線,西爾斯需要的門店越來越少,規模也越來越小。但西爾斯至今也未出現銷售業績和利潤強勁增長,誰會相信申請破產后,西爾斯能靠這種方式打翻身仗?雖然也曾有一些不錯的嘗試,比如為具體家電開設小門店,以及和亞馬遜合作,但顯然無力扭轉命運。 多年來,萊姆伯特還不斷為業績不佳找借口(2005年和去年都歸咎于媒體),最近怪起零售業大環境艱難。可今年卻是消費者支出最為強勁的年份,強詞奪理的借口實在沒法讓人信服。 萊姆伯特在2006年的致股東信中暗示,希望通過收縮業務規模恢復西爾斯的經營狀況:“如果門店的財務狀況良好且保持盈利,降低銷售并無裨益,但如果盈利不是主要目標,銷售主要來自分發產品而非直接向客戶提供價值,縮減銷售就有望實現經營成功。” 但是,問題就在這里:自從進入新時代,百年零售品牌西爾斯就未真正實現向客戶提供價值。(財富中文網) 譯者:Pessy 審校:夏林 |

What’s behind this chronic deterioration? Sears never gave shoppers a reason to keep going there, nor did Kmart, which incredibly was a larger retailer than Walmart only 30 years ago. The company also let too many stores fall into disrepair even as companies like Target, Walmart, and Home Depot (to which Sears has lost a lot of its appliance business) have invested heavily in their stores and the technology they use in them. With its once dominant catalog business, Sears had what it needed to win the e-commerce wars. Talk about throwing away a big lead. On the merchandise side, Sears has not been nearly as active as its rivals have: Other than the ill-fated Kardashian Kollection a few years ago, who remembers any Sears apparel? Lampert, who has long been promising improvements that have failed to materialize, has stuck to the line that Sears was reinventing itself as a membership-based retailer focused on its ShopYourWay loyalty program, therefore needing fewer and smaller locations. But those haven’t led to stronger sales or earnings results yet, so what’s the case for believing they’d help a post-bankruptcy Sears? The company has made some good moves, including launching some smaller-format appliance-specific stores as well as teaming up with Amazon. But those are clearly not moving the needle. Indeed, Lampert has trotted out countless excuses (including blaming the media last year and also in 2005) for years, most recently naming a difficult retail environment, a my-dog-ate-my-homework-caliber excuse that doesn’t wash in the most robust consumer spending environment in years. He hinted at shrinking Sears back to health in a 2006 letter to shareholders: “While reducing sales is not a prescription for success on a base of healthy, profitable stores, it can be a prescription for success where profit was not the primary objective and where sales came from ‘giving product away’ rather than from providing value to the customer.” But therein lies the rub: Sears in the modern era has never truly found a way to provide value to its customers in a competitive way. |